Good morning and happy Monday!

A quick administrative note: the Economic nSight report will not be published next week, Monday, September 4 in observance of Labor Day.

Let’s look at this past week’s major data points:

Keeping up with global economic data is a monumental task. With a financial planning and investment management firm to run, that is committed to doing our own independent research, we are forever grateful to the many excellent Economic aggregation resources that take the work out of gathering this data for us each day. They don’t give us analysis – that’s our job – but just compiling this information can be a full-time job. We want to give a big shout-out (and a thank you) to MacroMicro, TradingEconomics, and The Daily Shot. Though we use several more, these are three of our favorite places to see a daily aggregation of economic data, and you’ll often see their charts used here.

- At the Top: Jackson Hole and the state of inflation

- Housing update

- Jobs update

- Manufacturing update: Stagflation

- Consumer & credit update

At the Top:

Jackson Hole & the state of inflation

The Federal Reserve Board met for their annual conference in Jackson Hole, WY last week, and everyone was waiting to hear from Chairman Jerome Powell on where he thinks interest rates will peak. Powell, correctly in our view, noted that inflationary pressures continue to mount and inflation looks to be trying to move upward again. He stressed the Fed’s commitment to getting core inflation to 2% (it’s more than double that right now), which likely means more interest rate hikes.

One thing to note here is that there is a significant lag between a change in the Fed Funds rate (the shortest-term rate in the country’s economy) and its broader economic impact. Most economists believe it’s a 9-12 month delay before each rate hike will really show its impact. With that in mind, we are experiencing an economy that hasn’t yet been impacted by even half of the rate hikes we’ve experienced since March of 2022. We expect to see the economy begin to rapidly slow down in the coming weeks.\, and are already seeing some of this in housing, jobs, and manufacturing. This week, however, even the service sector, which has been pretty resilient so far, is rapidly slowing down.

What this means to you

All roads point to a recession. I wish there was better news to deliver, but we are 100% convinced, based on objective economic data, that the economy remains on a course toward a slow-down, and that market participants are, at best, being obstinate in the face of a reality they don’t want to accept. With the reintroduction of student loan payments next month, I believe that consumers will finally be fully “tapped out” and we will, unfortunately, see collapsing spending on discretionary goods and services (those things you can live without if you have to), and rising credit card and loan delinquencies (we’re seeing some of this already – see below). Student loans returning just as inflation begins to climb again (causing more rate hikes) will crush what’s left of private consumption, and the recession will begin in earnest.

Things happen slowly in economics until they don’t. We’ve been warning our clients and positioning our investment models for this for over a year now because the economy gives off lots of warning signs that something is wrong. You either heed those warnings, or you become one of the masses of people who will be saying in the coming weeks that the “sudden downturn” was “unexpected”. It was never unexpected – it was just in the way of the herd’s strong desire for it not to be true. As you’ll hear me say often if you are a client – the data is the data – it doesn’t care about politics or fads – it just IS. And investors will find out once again, as they do every single time a recession arrives: you can only pretend gravity doesn’t exist for so long.

Housing Update

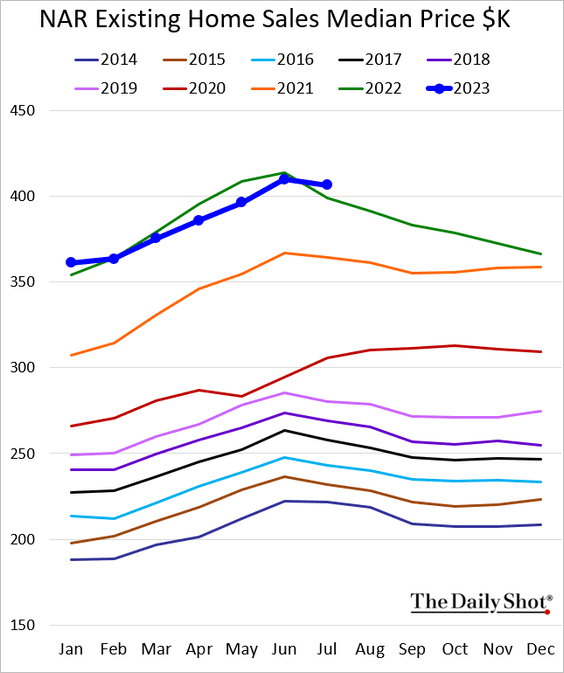

Other than jobs, I don’t think we get more frequent updates on a particular part of the economy more often than housing. Every week it seems, we have updated insight on this most important sector. Interestingly, I’ve noticed a stark uptick this past week in the number of social media posts about housing and the lack of affordability for Millennials and Gen Z. They are absolutely correct: the surge in house prices the past few years, which we’ve documented extensively in previous reports, is in an unsustainable bubble, and like all bubbles, this one will also “pop”.

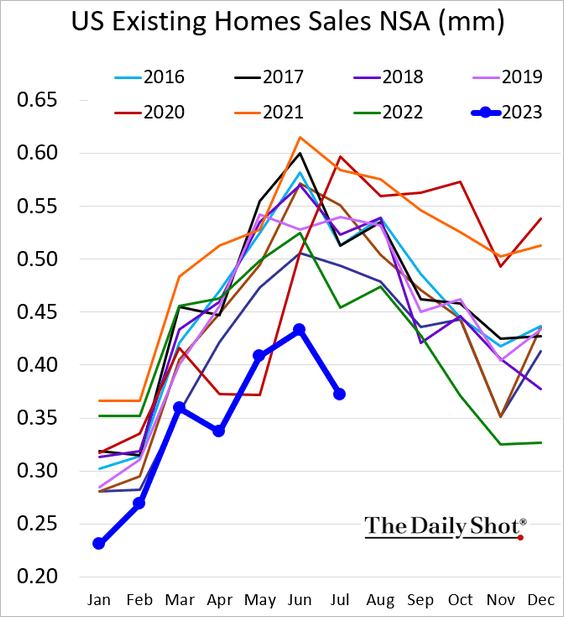

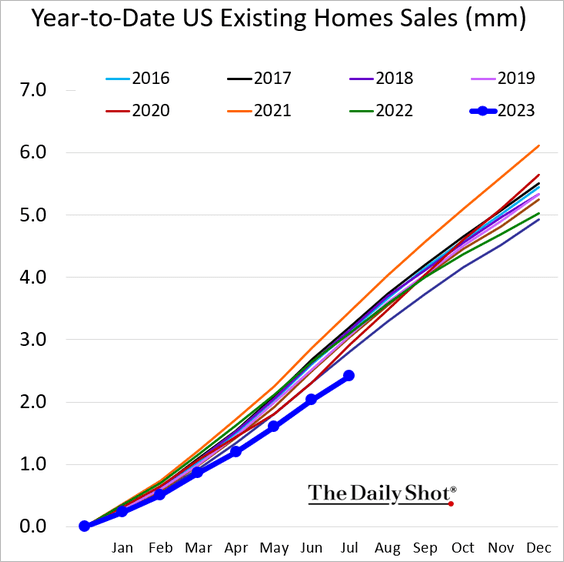

First, let’s look at mortgage applications as the leading indicator of where housing is ultimately headed (you can’t just keep making houses forever if no one is buying them). Mortgage applications are deeply below all previous years in the last decade. Mortgages are seasonal – people move mostly during the summer months, so it’s common to see mortgages and home sales peak May- August and crash out during the winter. This year is following a seasonal trend but is well below previous years.

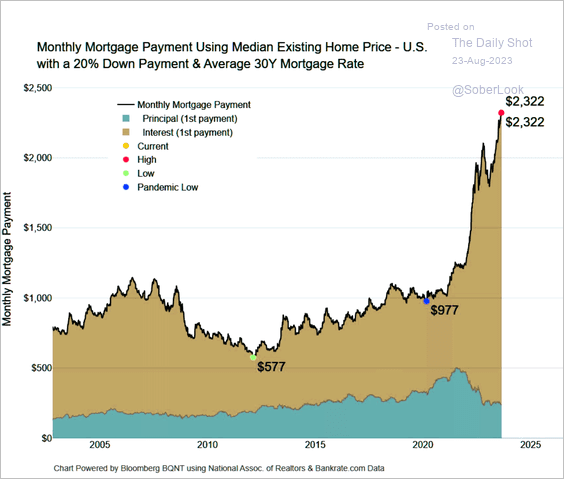

The reason for that is the combination of interest rates being so high as the Fed fights inflation, plus the preposterous spike in home prices since about 2019. A family buying the average home in 2013 at current interest rates would have a $577 monthly payment. In 2020 it nearly doubled to $977. However, just 3 years later, it climbed a whopping 73% to $2,322. This is obviously unsustainable, and one of two things MUST happen – either interest rates collapse so that home payments are affordable, or home PRICES must collapse. We believe, with a recession looming, it will be home PRICES before it is interest rates.

Yet despite the fact that no one is obtaining a mortgage at least right now, home builders continue to crank out new houses. This is, again, not sustainable. The market is building homes it cannot sell (at least to individual families – investors in real estate are a major reason house prices have spiked so significantly – more on that in a moment):

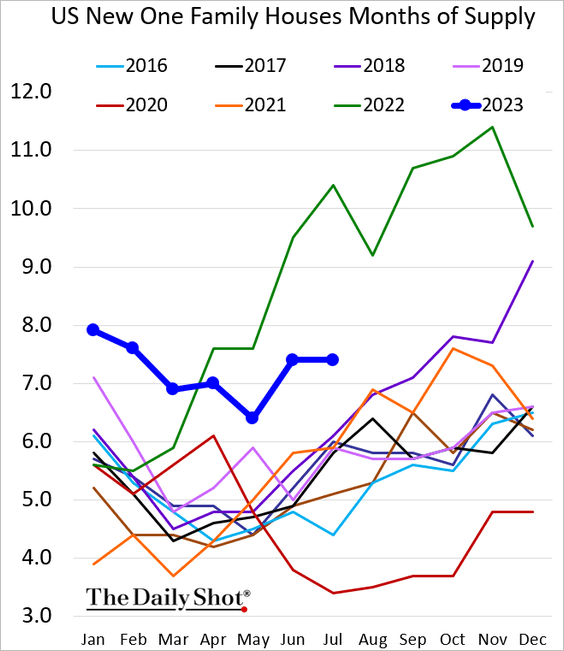

New home inventory is near decade highs – meaning, we’ve built too many.

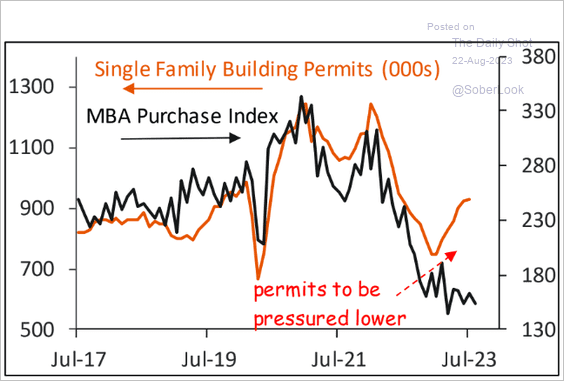

There is usually a tight correlation between mortgage applications and how many new homes are built (obviously). But since last year, that has gone wildly askew. It cannot be sustained. There cannot be houses built indefinitely if no one can qualify for a loan to buy them.

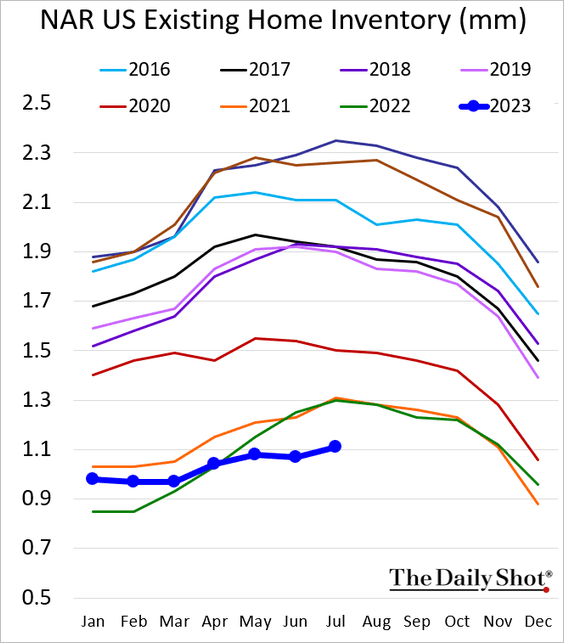

They’re doing this, however, because the inventory of EXISTING homes for sale is at all-time lows. This has to do with the historically low interest rates we experienced during Covid. Many homeowners refinanced their home loans or purchased bigger homes (including my wife and I), locking in interest rates as low as 2.5%. Those people cannot replace their current home loan with anything close to what they had before, so even though home prices have soared since Covid (our new home has almost doubled in value in just 3 years), there is little incentive to cash out and sell these homes for two reasons: no one can afford the mortgage payment on the home you’re selling, and your next home will be similarly inflated in price but with a MUCH higher interest rate to go with that new loan. So, sellers aren’t putting their homes up for sale. Not yet.

That lack of supply is one of the few things keeping home prices up right now. Demand has utterly collapsed because of the combination of high prices and high borrowing rates.

But the lack of sellers has kept prices up. For now.

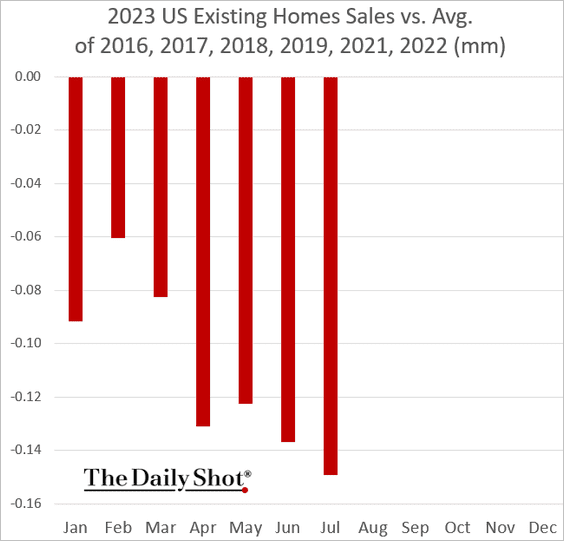

Another look confirming existing home sales are at decade lows (and the gap is widening):

Compared to the average for August of the last 6 “normal” years (2020 excluded), we’re 15% off of existing home sales, and it’s getting worse. This is a collapse in the real estate and mortgage industries.

Here is the other major reason for the spike in home prices to begin with: families didn’t buy them all – INVESTORS are almost 25% of the buyers of American homes. Bought to be used as income sources from either long-term tenants or as AirBnB-type rentals, and sometimes even just to “flip” them in this unsustainable housing bubble, the inventory of homes was made artificially small due to so many investors who were not going to ever occupy the home as its residents.

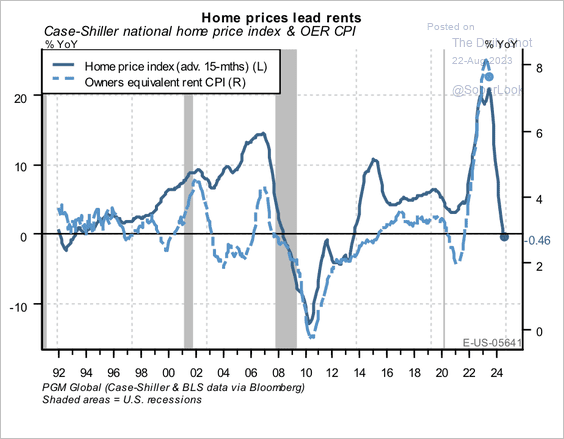

Unfortunately, that means people who would otherwise buy a home of their own are forced to rent for now. This graph shows that the high demand for homes to rent has also kept rent rates up at all-time highs (and it accelerated again in the past few months). Even though the rate of increase in rent is slowing (black line), it still means rents are rising

Thankfully, as home prices do come down (and they will), rent inflation will follow.

What this means for you

The housing market is currently in a bubble far worse than we experienced in the last recession, which was almost entirely caused by housing/mortgage shenanigans. I believe we are headed for a significant housing market decline in the coming months. Clients who are interested in buying a home or a second home may very well have the opportunity to do so at dramatically better prices in the next 18-24 months, but other clients who are interested in selling property may have a long time to wait for those home prices to return. Our macro models are not invested in either real estate or mortgage/property finance at this time.

Jobs Updates

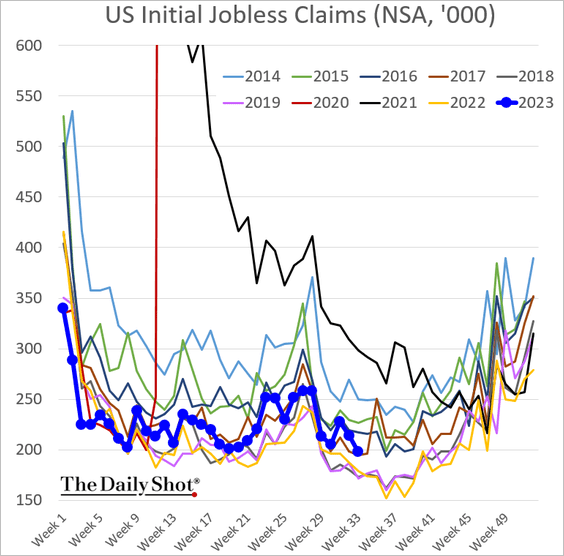

We look at jobs regularly, and the current trajectory remains unchanged. Initial claims, while still low, are trending higher, and continuing claims remain my most persistent worry. This week’s initial jobless claims came in slightly below expectations, though trending against historical trends. This week, we have a couple of other significant bits of data that sheds better light on where we’re headed.

First, initial claims for unemployment were lower these past two weeks but I am leery about the accuracy of the data, because ever time we saw a significant drop in initial claims this summer, it was due to one state removing a huge number of claims at once, claiming it was removing “fraudulent” claims. To remove them from INITIAL filings instead of continuing filings doesn’t make sense to me. Did hundreds of thousands of fraud cases show up in the same week? No, or we would have seen major spikes in initial claims which we have not seen.

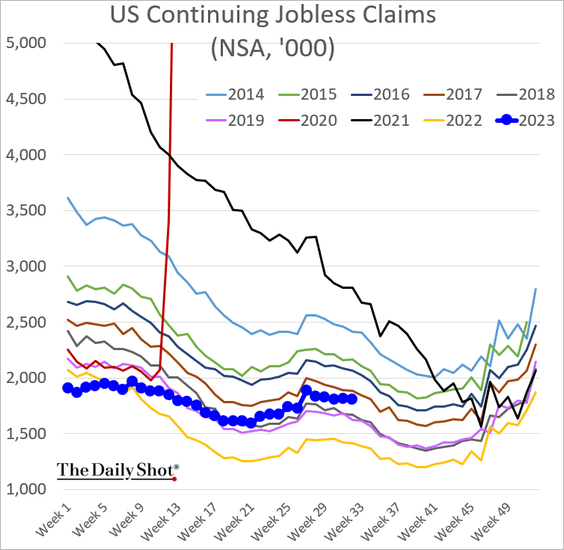

As we’ve said many times, however, it is the CONTINUING claims that matter most to our analysis. It’s one thing to lose a job, but if you lose one can cannot find a new one quickly, that says much more about the state of the economy. Continuing claims, while still low, are trending against seasonal norms:

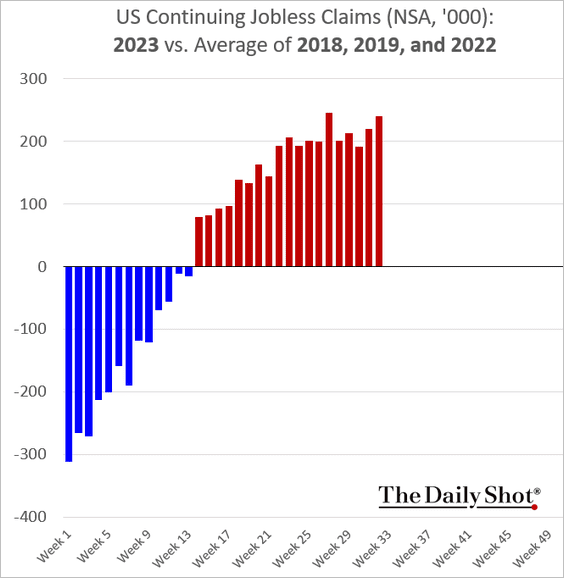

And when we look at the continuing claims vs. an average of the same week in the last 3 “normal” hiring years, we can see the trend is uncomfortably up and headed in the wrong direction:

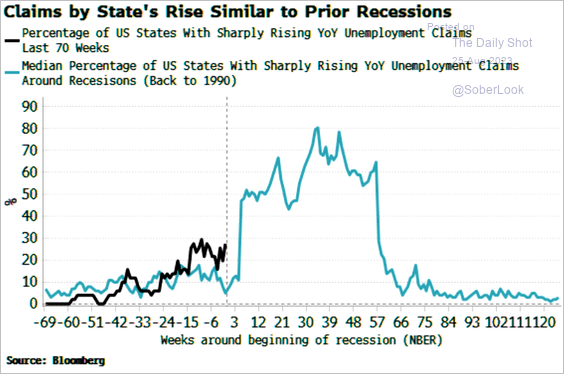

There is another way to see whether the numbers are being skewed by unusually strong hiring but only in some states. If we look at the number of STATES with rising cases of unemployment (instead of a total headcount nationwide), we can see a much more concerning trend. The black line is the percentage of states with rising unemployment claims. The blue line is the average of this same statistic from all recessions going back to 1990.

This tells us a number of things. All things being the same, we are very likely at or within weeks of actually entering a recession. It also shows that unemployment doesn’t just meander up and back down again – it surges. Unemployment, if it follows the historical trends into this next recession, will suddenly spike up across the states much more evenly, plateau off for as much as a year, and then surge back down again as things pick up.

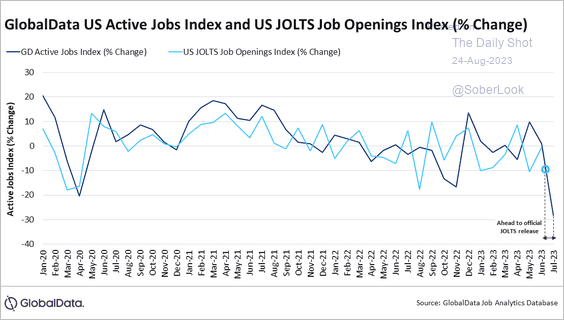

We can also see from published job openings (which has been rapidly dropping this summer) that employment opportunities are quickly drying up:

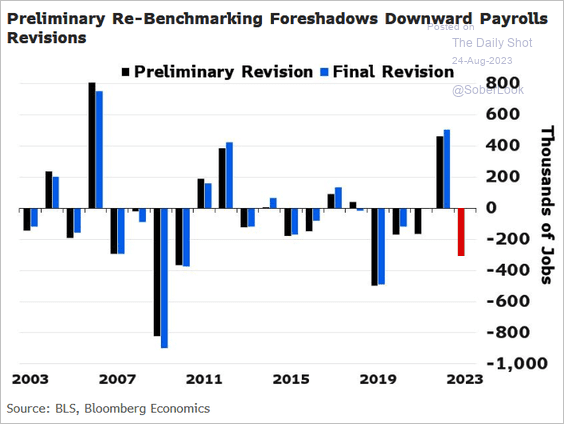

This past week, we also got revisions to previous jobs numbers. Revised job estimates were about 300,000 lower than previously reported. This is common, as you can see from the graph that it is much more likely to have had initial jobs numbers be overly optimistic than not (revisions tend to be downward). Take note of the area between 2007-2011, which was our last recession. Jobs numbers were revised down by nearly 1,000,000 in 2009, but we are right at where the jobs numbers were first revised down in 2007.

In fact, 2006-2007 looks VERY similar to 2022 and 20223 so far.

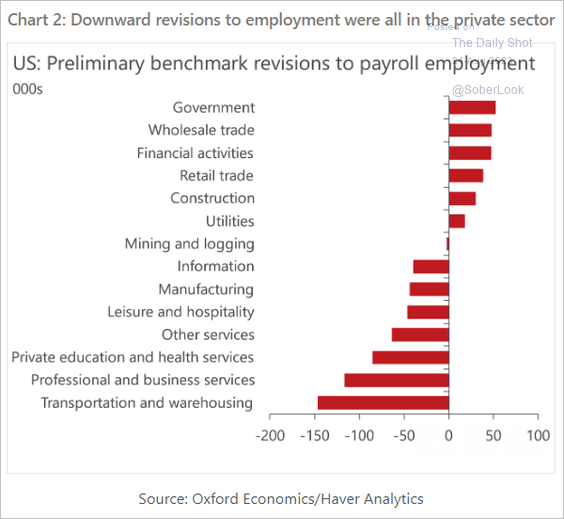

Also of note, in those 300,000 jobs that were over-reported and needed to be revised down, all of them were in the private sector, with both manufacturing and service jobs being affected pretty evenly. The one that hired more than anyone thought? The government.

What this means to you

The job market is showing much more obvious signs of strain. Sadly this will get worse as we head into a recession – that’s an economic certainty and one the Federal Reserve is actually trying to achieve without too many job losses. We urge our clients to reduce their debt load and increase their personal savings, and keep investments conservatively positioned for now. A recession doesn’t mean the end of the world, but it does mean seeing our unemployment rate climb from its current 3.5% to maybe 5.5% or 6.5%. That means, sadly, a lot of lost jobs and financial hardship for many families, so please take the risk of job insecurity seriously.

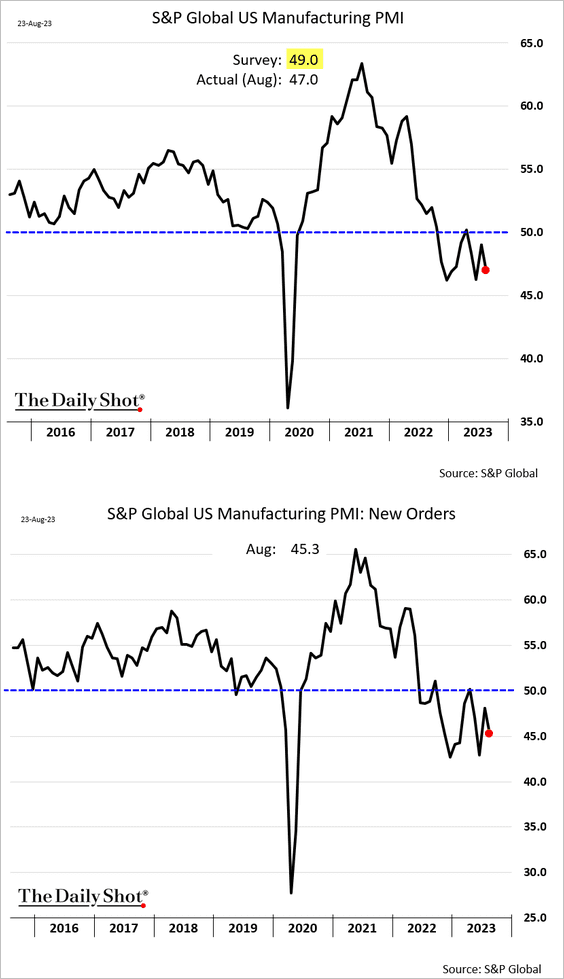

Manufacturing Outlook: Stagflation

The S&P Global (meaning: all of the United States) PMI reports for July showed a downturn again in both Manufacturing and Services. Manufacturing has been in recessionary territory since the middle of 2022:

…while Services has held on for the most part. It looked like Services was rebounding after bottoming last year, but has been turning down again for the last quarter:

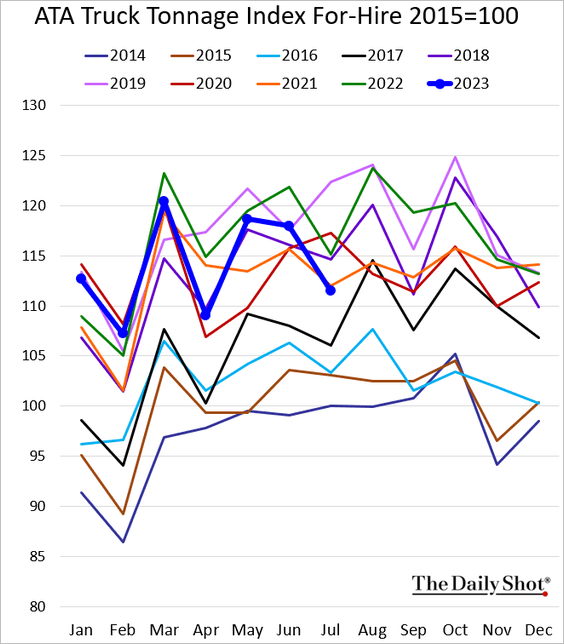

In addition to assessing what’s already happened (PMI reports are always backward-looking), it is also important to look at current indications of economic activity. We are also seeing a decline in the tonnage for freight shipping as the year progresses, also. Here we see tonnage, while still relatively strong, is trending lower and is the fifth-lowest out of 10 years so far.

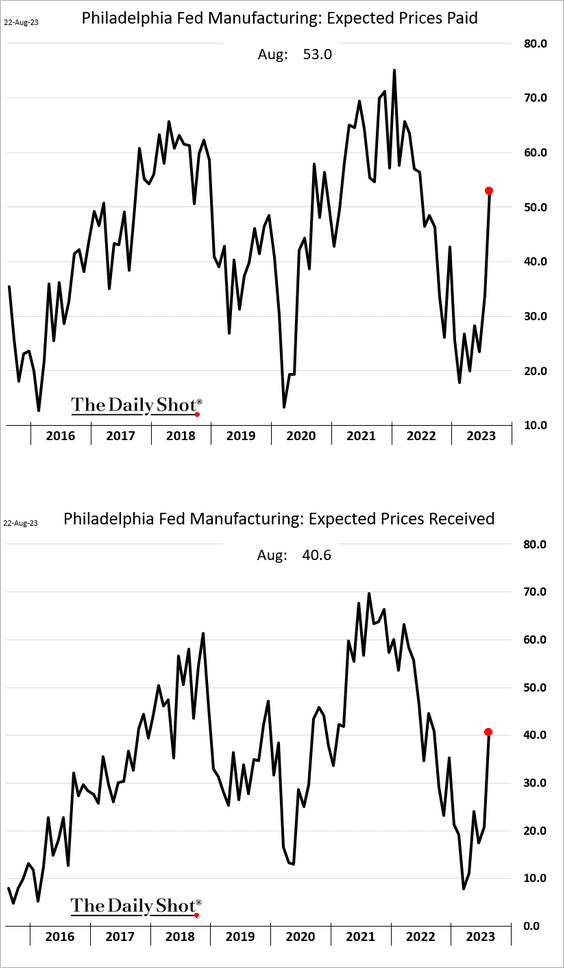

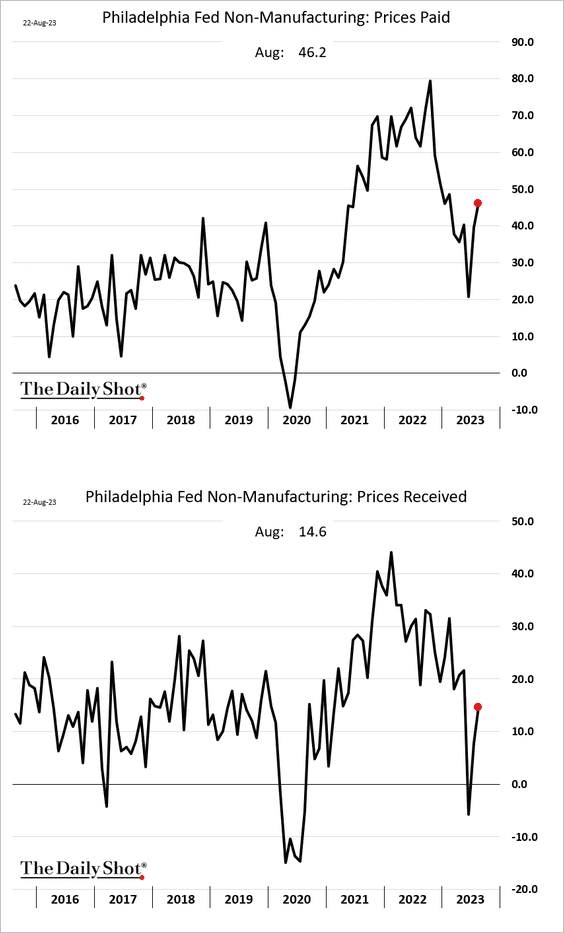

What is most concerning to me as an analyst of these manufacturing reports is the nearly universal indication that inflation is returning in a pretty rapid and aggressive fashion. Chart after chart from companies across the nation indicates that prices are rising on their raw materials and wages. Companies are expecting to pay more, and to charge more:

The economic condition where you have declining (or stagnant) productive output, combined with increasing prices is called STAGFLATION. It can be argued that stagflation is the worst of all economic conditions. It may be too early yet to determine of inflation truly is returning for another ugly rise, but if it is, it is happening even though demand for products and services is slowing down. This would be the definition of a stagflationary environment.

What this means for you

We are 100% certain that a recession is imminent. We’ve said this for many months now. We believe we are on the cusp now, and as the data bits below regarding consumer financial health will indicate, we are very likely about to see significant reversals in several of the investment markets. Our clients remain very conservatively invested in our defensive, macroeconomic data-dependent models, and we are watching for opportunities to improve safety and increase yields on a weely basis.

Consumer & Credit Update

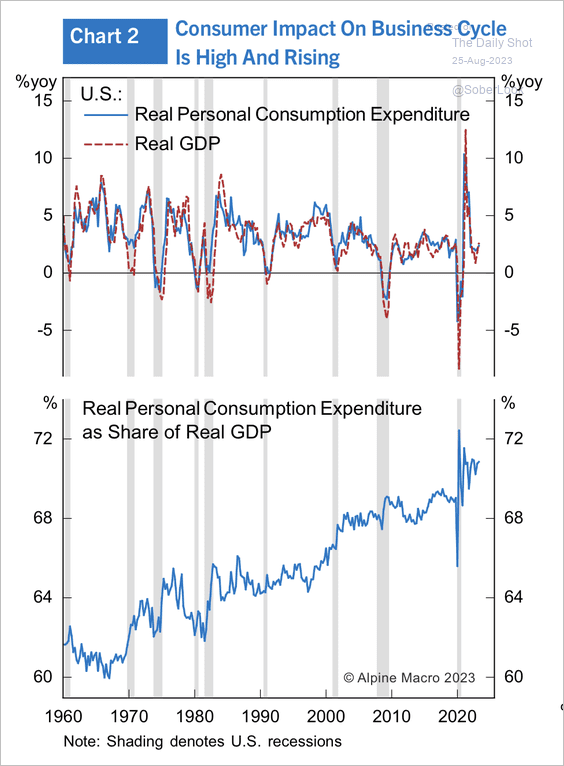

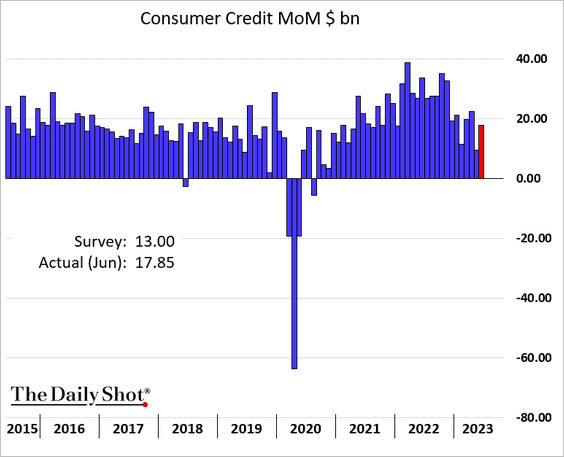

Finally, we have a smattering of diverse “hints” around consumer spending and bank credit to give us a better picture of where we are headed. Remember that 70% of our entire economy depends on private consumption – that is, you and I spending our paychecks. If the consumer is not in a place able to buy products and services, because of job insecurity, high taxes, or inflation, the economy will suffer.

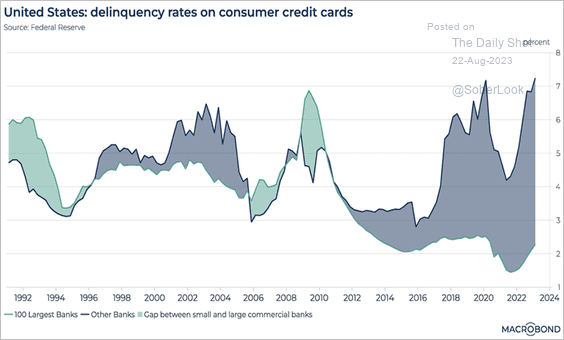

First up: credit cards becoming delinquent. While still below the worst of the 2008-2011 recession, our credit card delinquency rates have now climbed to the same level as the early days of that recession, and well above the financial challenges related to Covid:

By far, the banks most affected by the climbing delinquency rates on credit cards are the smaller community banks. The gray shaded area is the difference between the delinquency rates at small banks vs. delinquencies at large ones.

This is happening just as student loan payments resume in October. Consumers enjoyed higher savings rates during and shortly after the Covid pandemic because of all of the stimulus spending (and nothing was open to go spend it), but those savings have largely been depleted now. Most estimates are that the excess savings from Covid fiscal policies were finally exhausted in July.

The sudden downturn in so many economic indicators has turned the Economic Surprise Index on a downward trajectory:

And consumer sentiment, which had seen a couple of months of recovery as inflation eased, reversed and came in below expectations (2 charts):

As I mentioned, the consumer has a very large impact on the overall economy, so as consumers have less and less extra money to spend, things crash for business very quickly:

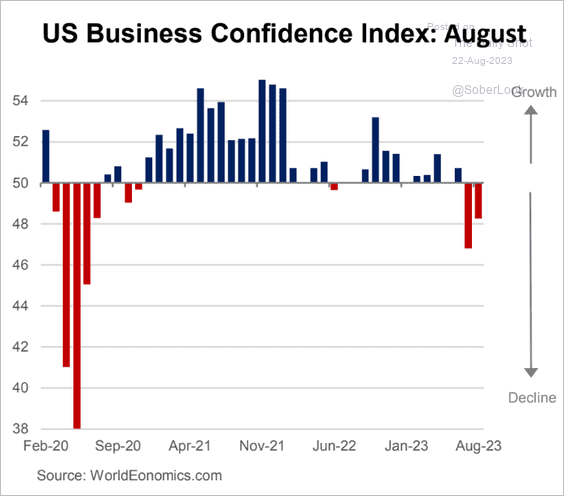

And so, unsurprisingly, when consumers pull back, business confidence drops. This can become a bit of a self-fulfilling prophesy because as business sentiment drops, any plans for expansion and hiring will also slow down, which may increase the negative sentiment of the workers. This feedback look can itself turn into a recession:

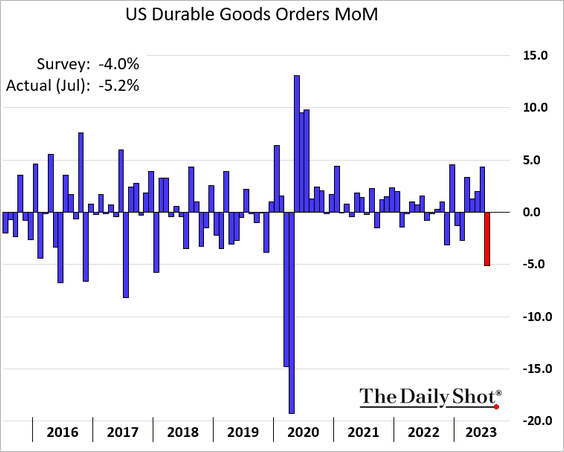

As a result, durable goods orders dropped unexpectedly:

Indeed, it looks like business orders have peaked. What is interesting to note is how much inflation has affected spending for businesses, too: the black line, which is flat all year, shows how much companies have spend on capital goods orders, but that includes the elevated prices due to inflation. The blue line shows what companies have actually bought. So we’re buying much less than we were a few years ago, we’re just paying MUCH more for it.

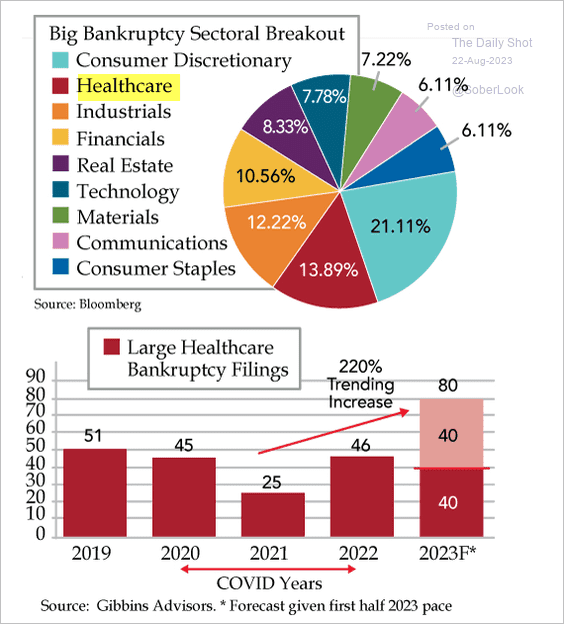

We’re also watching business bankruptcies very closely because we’ve seen a big uptick in them in the past few months. A surprise this month was the high number of large healthcare companies that filed for bankruptcy protection, more than double the number since Covid.

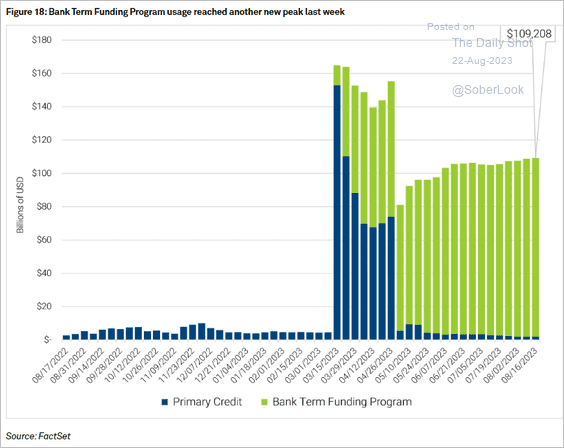

And we are seeing signs of bank stress. This chart shows the borrowing banks are doing from the Federal Reserve in order to meet their reserve requirements. A bank that cannot meet its reserve needs is considered insolvent and would be taken over by the FDIC. Since the spring of this year, when the Federal Reserve opened an emergency line of credit for banks (the green bars), the use of this program has skyrocketed, and concerningly, is actually increasing each week now:

And for clients who wonder why we are still so defensively invested in our models, I present this chart, that shows the low of money into and out of different funds. Here you can clearly see what we call “herd mentality” in full force. Massive amounts of money is flowing into the technology sector, exclusively. Because the NASDAQ and S&P 500 have so many tech companies in their indexes, these indexes have looked to be healthy for most of 2023. However, a closer inspection shows deterioration across the entire economy… EXCEPT tech stocks. We believe this rally is unsustaniable and not realistic because tech stocks operate in the same economic environment as the remaining 10 sectors, and that this bubble, like all bubbles, will finally burst.

What this means for you

We remain conservatively invested and allow the economy to direct our decisions, not market sentiment and herd bias. The data clearly shows, from nearly every angle we can find, a deteriorating economic environment, and our clients are correctly positioned for protection against, and even the possibility to gain from, the coming downturn.

Bottom Line:

Download our brand-new E-Book “7 Hacks To Recession-Proof Your Financial Life” today.

We remain convinced that a recession is imminent, even as the market fights back hard against it. Do not let the current market rally fool you – there is no sustainable way to grow profits (and therefore a supportable stock price) in an economy that is rapidly losing steam. Corporate profit reports are backward-looking and economic projections are forward-looking. Do not be lulled into complacency just because the stock market allows itself to.

We’ve been alerting our clients for nearly two years now that inflation was going to cause significant problems and our central banks would have to take progressively stronger actions to combat it. That appears to be a correct call.

No one knows exactly when a recession will be declared, but we firmly believe most of the larger economies of the world are right at the door of one now. Recessions can take years to recover from, which is why we believe it is vitally important to get your family and business finances ready to weather through such a storm.

We predicted the beginning of a turn in the current market rally last week, and we reiterate that sentiment now. There will always be market movement that runs counter to the economic data because markets are much more short-term focused, and let’s face it: until fear takes hold, greed is the prevailing emotional state of most market participants. We do believe, however, that the recent rally has fully run its course, and there will soon be a strong shift from stocks into safer investment options such as corporate and government bonds. With interest rates this high, getting a 5% or better yield, risk-free is becoming a more and more attractive option for investors concerned about the coming economic uncertainty. Once there is consensus that either the economy is earnestly deteriorating, or the Fed announces the end of rate hikes, the move from stocks to bonds will accelerate.

Whether you are our client or not, you need to consider the broader economy (and much less so the daily market fluctuations) when making investment decisions. The economy is telling us clearly what is coming, and you need to have your investment accounts prepared before that happens.

Just this past spring, I published an ebook to help you get your finances ready for the recession directly ahead. It’s yours totally free. Just click on the book image to access and download it.

Use these economic reports, and those of others working in this space, to prepare. You can not only avoid much of the pain that is coming, but you might actually profit from it, if your investments are properly positioned, and you’ve done what you can to shore up your business’ and family’s financial situation. If you need help with this, nVest Advisors has amazingly affordable personal financial planning and fiduciary investment management services to help you.

This is what we do for a living, and we’re very happy to partner with you on that endeavor.

Reach out to us for a totally free financial and portfolio checkup today if you’re concerned about where your finances sit for the coming few years, particularly if you are at or approaching retirement age. We’re delighted to offer you our thoughts. You can schedule that time with us below:

Watching This Week:

- Jobs Report

- Service Sector Update

- Commodities

Jeremy Torgerson, CEO, CIO & Senior Advisor

{kind=link}