Good morning and happy Monday! The ongoing conflict in the Middle East is causing significant economic damage to the area, but the human toll is the one we should always keep in our hearts and minds. War is hell; we grieve for the many innocent people on both sides who will suffer because of it and we pray that it ends quickly.

Now, let’s get on with economic indicators for last week:

Keeping up with global economic data is a monumental task. With a financial planning and investment management firm to run, that is committed to doing our own independent research, we are forever grateful to the many excellent Economic aggregation resources that take the work out of gathering this data for us each day. They don’t give us analysis – that’s our job – but just compiling this information can be a full-time job. We want to give a big shout-out (and a thank you) to CurrentMarketValuations, FRED, MacroMicro, TradingEconomics, and The Daily Shot. Though we use several more, these are three of our favorite places to see a daily aggregation of economic data, and you’ll often see their charts used here.

- nFocus: Inflation

- Jobs Update

- Real Estate Update

- Small Business Update

nFocus: Inflation

Both the Producer Price Index (PPI) and the Consumer Price Index (CPI) numbers came out last week, surprising many analysts with higher than expected reads, particularly in the CORE (we’ve discussed this in great detail over the past several months), and in Services.

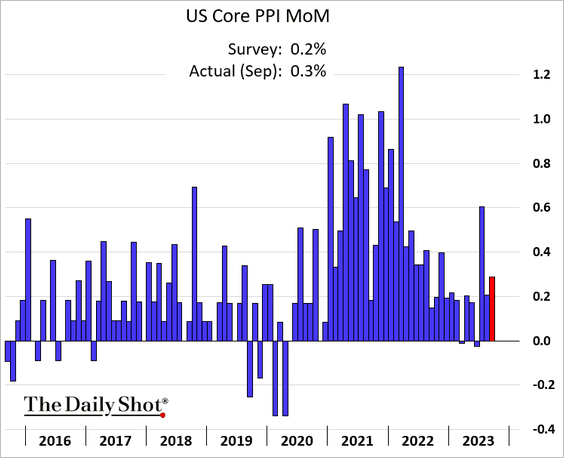

First, the US PPI came in at 0.5% above the previous month, indicating that prices to manufacture goods and offer services to retail consumers is climbing again. This is the third straight month-over-month increase in prices and gives us concern that inflation is resuming. We will see in a moment that this is a common occurrence during historical inflationary cycles after massive government spending – inflation tends to run in waves over and over again before they’re finally beaten either by extreme monetary and fiscal changes, or a recession does the work for the government.

The CORE PPI (those most-often recurring expenses that companies have to pay in order to do the work they do for consumers), increased again, as well, passing experts’ guesses by half. This means that the inflation is not temporary or that only part of their prices are going up; inflation is affecting business costs across the board.

CORE PPI excluding trade services also showed an increase, meaning that it’s not just other companies passing on price increases to their customers; it is the cost of raw materials and other supplies doing the work, as well.

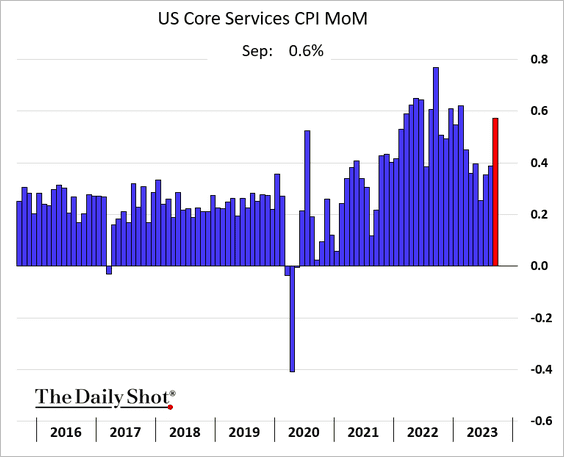

All of this eventually gets passed down to the consumer – you and me – and can be measured by the CONSUMER Price Index (CPI), which came out a day after the PPI for the month of September. The CPI shows the same issues as PPI – that prices are increasing again on both businesses and consumers. The CPI for September shot up an alarming 0.4% in September, and CORE inflation ( the stuff we can’t do without each month) was up 0.3% over the month before. What is concerning is that though the trend is down, Wall Street investors and economists sincerely believed they had beaten it and were pricing in a stock market rally as a result.

Perhaps the biggest surprise was the Services CPI, which came in the highest in over six months, meaning all of the non-product things we pay for (subscription services, health care, airline tickets, etc. are where a lot of inflation is presently happening.

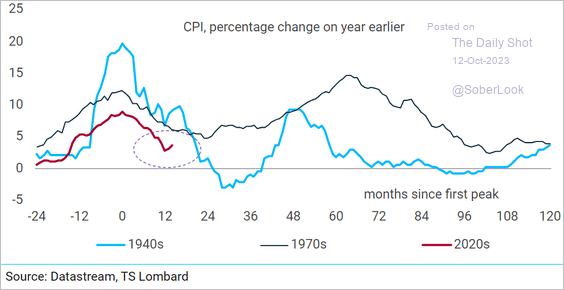

One thing I’d like to point out is how inflation cycles operate in history, and though history never repeats itself exactly, it can often run very similarly to what it’s done before. Analysts love saying, “this time is different,” but in terms of what moves an economy, it seldom is.

The graph below shows the last three long-term inflationary cycles in the U.S. economy, the 1940s in blue, the 1970s in black, and our current cycle in red. As you can see, in both previous cycles, inflation went up, dropped off (and gave the false impression that it was finished), and then rose again to cause greater problems. You can see the number of months along the bottom axis of the graph. What we are experiencing is EXACTLY what an inflationary wave cycle would do.

We are watching this closely, but we do not believe inflation is finished, and it may mean that the Federal Reserve will have to do much more in terms of high interest rates and quantitative tightening in order to actually fix this problem.

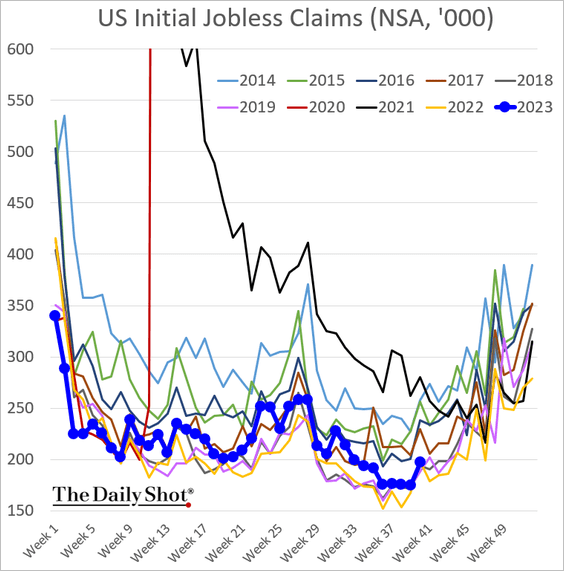

Jobs Update

Jobs numbers are something we get weekly from the Bureau of Labor Statistics, and monthly from other sources like ADP. I am now officially leery of the BLS statistics for a variety of reasons, and so are many economists who cannot reconcile the wide disparity between what the GOVERNMENT says hiring is doing, and what COMPANIES themselves are saying.

However, the official BLS numbers for last week show us that employment is still tight but have started to tick up noticeably in the past week:

Because hiring is seasonal, it’s helpful to look at the same week of the year vs. the average of that same week in previous years, to see if there is an outlier. What this tells us is that initial claims have been marginally higher than the last 3 “normal” years in the same week, for almost all of 2023.

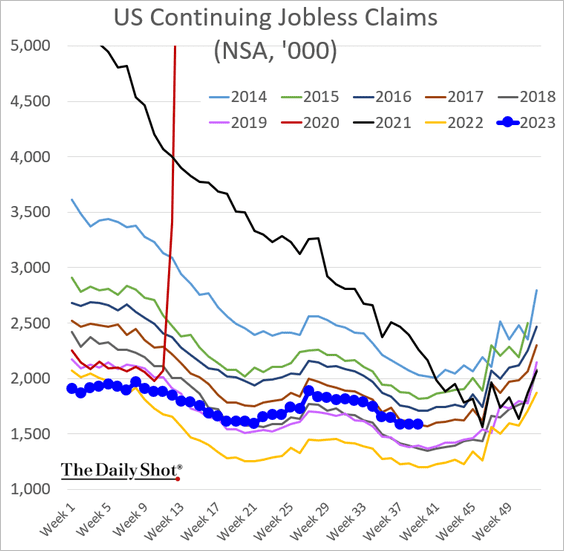

But as I’ve said many times, it is the CONTINUING claims that we need to pay more attention to, because these are people who have lost their jobs, have worked through whatever severance package they were given, and now still cannot find another job. Continuing claims, while still low at the moment, have moved up across the graph of several previous years over the last decade, and are now about middle-of-the road.

When you compare the continuing claims to the last three “normal” years, however, we can see a strong trend toward more ongoing joblessness ahead:

What this means for you

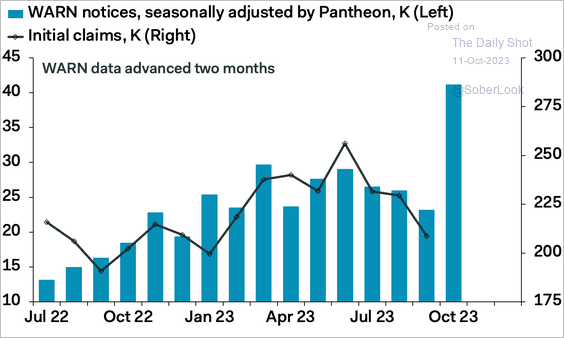

We continue to watch employment carefully but it is a lagging indicator in terms of predicting a recession. Hiring typically stays strong right up to the start of a recession, because laying people off is the very last thing most companies want to do (or even have to do). However, once sales drop off and hours have been reduced, job cuts always follow. We anticipate a sudden spike in layoff announcements as the recession gets underway. Indeed, companies with more than 100 employees who are required to give 60-day advance notice of a layoff jumped massively this month:

This tells us that higher unemployment numbers are imminent. If past recessions are any indication of what is very likely ahead, look at how fast unemployment claims shot up in each of the last 7 recessions:

Real Estate Update

We read a statistic this week that 60,000 realtors have exited the industry so far in 2023, and that there are still currently 2 realtors for every 1 home on the market. Real estate, particularly commercial real estate, has long been where we believed a significant amount of economic harm would be felt, and we are starting to see that happen now.

The average interest rate on a new 30-year mortgage climbed to 8% last week. This is simply crushing demand for home purchases and refinances. We will have much more about real estate next week:

Compared to the last 7 years average, by week, we can see that this year has been absolutely terrible for the mortgage business:

What this means for you

We continue to believe home prices will come down long before interest rates do. This is good news for home buyers but bad news for current homeowners. We recommend that you keep your debts minimal, clean up your credit score, and try to save as much as possible. If you are dealing with a high-interest mortgage that you though you could refinance by now, you may have to adjust your budget, as we anticipate that it will be another 1-2 years before you can refinance your home at a lower rate, and even longer if you have less than 15% equity in your home (because you may be “underwater” in terms of home equity).

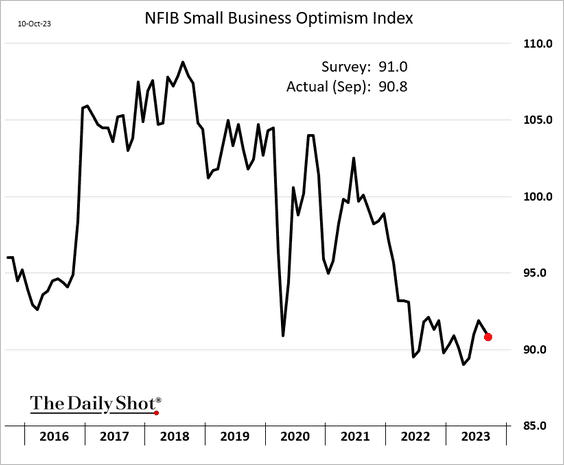

Small Business Update

Because they create as many as 75% of all jobs in our economy, keeping an eye on small business health is vital to any economic study. As has been the case for many months now, Small Businesses continue to report difficult conditions, though some have reported seeing a light at the end of the tunnel. We believe this may be premature and was largely related to cooling inflation over the summer, which has sadly, now reversed.

The biggest challenge small businesses are reporting is that it is getting harder and harder to find a loan and they are paying MUCH more interest to get the ones they can. Banks are tightening up their lending requirements on small businesses because during recessions, many small businesses aren’t able to endure 12-36 months of lower revenue, and therefore default on debts at a higher rate than larger businesses:

What this means for you

We see nothing to change our view of the worsening economic trajectory we’ve talked about many times in this space. Small businesses are the lifeblood of American jobs, and this is where we fear the layoffs that are NOT required to be pre-announced (see the Jobs Update above) will surprise market analysts.

Bottom Line:

Download our brand-new E-Book “7 Hacks To Recession-Proof Your Financial Life” today.

We remain convinced that a recession is imminent, even as the market fights back hard against it. Do not let the current market rally fool you – there is no sustainable way to grow profits (and therefore a supportable stock price) in an economy that is rapidly losing steam. Corporate profit reports are backward-looking and economic projections are forward-looking. Do not be lulled into complacency just because the stock market allows itself to.

We’ve been alerting our clients for nearly two years now that inflation was going to cause significant problems and our central banks would have to take progressively stronger actions to combat it. No one knows exactly when a recession will be declared, but we believe most of the larger economies of the world are right at the door of one now. Recessions can take years to recover from, which is why we believe it is vitally important to get your family and business finances ready to weather through such a storm.

We predicted the beginning of a turn in the current market rally last week, and we reiterate that sentiment now. There will always be market movement that runs counter to the economic data because markets are much more short-term focused, and let’s face it: until fear takes hold, greed is the prevailing emotional state of most market participants. We do believe, however, that the recent rally has fully run its course, and there will soon be a strong shift from stocks into safer investment options such as corporate and government bonds. With interest rates this high, getting a 5% or better yield, risk-free is becoming a more and more attractive option for investors concerned about the coming economic uncertainty. Once there is consensus that either the economy is earnestly deteriorating, or the Fed announces the end of rate hikes, the move from stocks to bonds will accelerate.

Whether you are our client or not, you need to consider the broader economy (and much less so the daily market fluctuations) when making investment decisions. The economy is telling us clearly what is coming, and you need to have your investment accounts prepared before that happens.

Just this past spring, I published an ebook to help you get your finances ready for the recession directly ahead. It’s yours totally free. Just click on the book image to access and download it.

Use these economic reports, and those of others working in this space, to prepare. You can not only avoid much of the pain that is coming, but you might actually profit from it, if your investments are properly positioned, and you’ve done what you can to shore up your business’ and family’s financial situation. If you need help with this, nVest Advisors has amazingly affordable personal financial planning and fiduciary investment management services to help you.

This is what we do for a living, and we’re very happy to partner with you on that endeavor.

Reach out to us for a totally free financial and portfolio checkup today if you’re concerned about where your finances sit for the coming few years, particularly if you are at or approaching retirement age. We’re delighted to offer you our thoughts. You can schedule that time with us below:

Schedule a Free Q&A Call with Jeremy Now

Jeremy Torgerson, CEO, CIO & Senior Advisor