Click to expand.

Good morning and happy Monday! Our hearts are heavy this morning after the surprise attacks on Israel on Saturday, and the resulting military conflict currently underway. Our prayers are with the victims and their families. We will discuss the implications to the global economy briefly in today’s report.

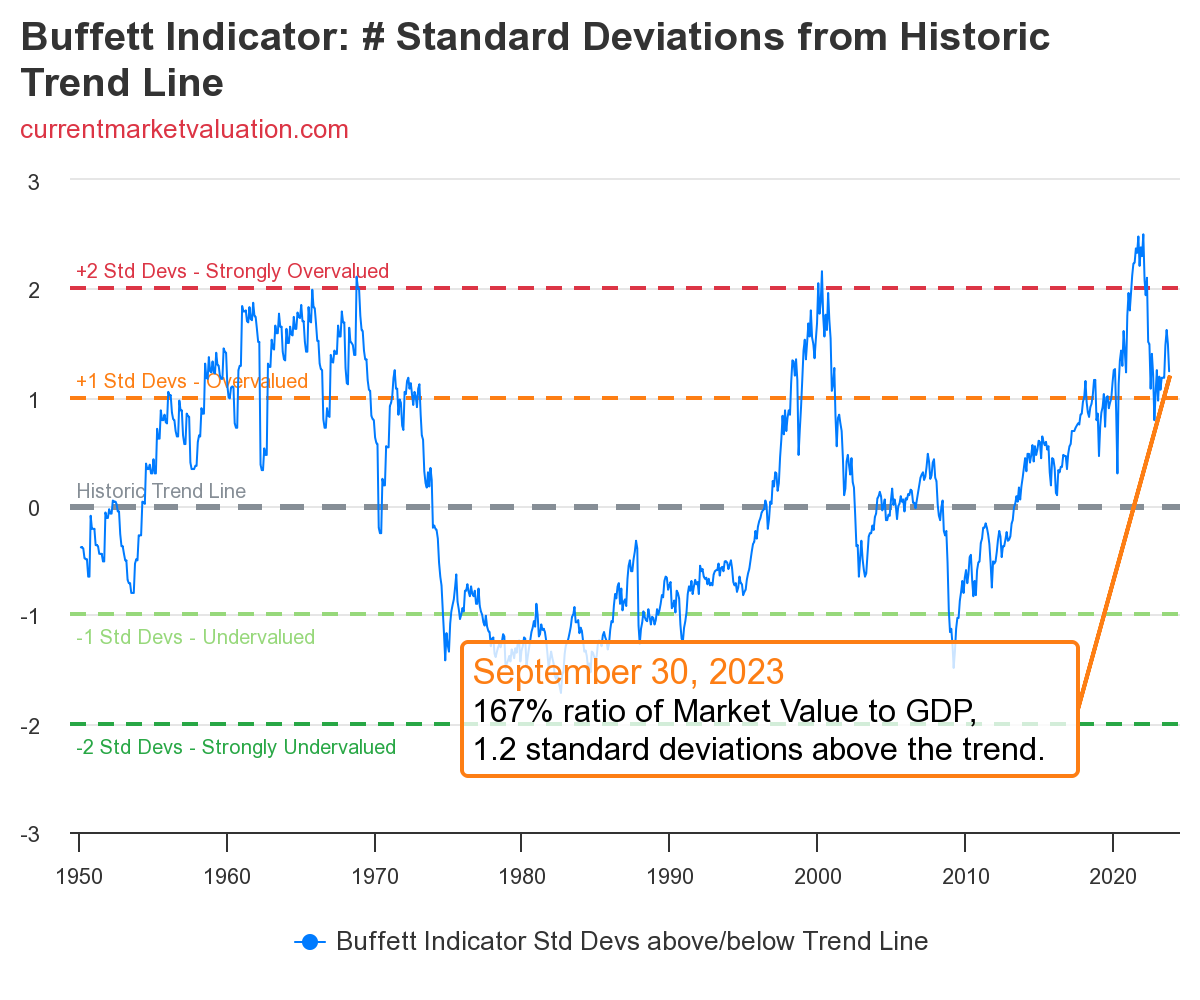

Current BUFFETT INDICATOR: OVERVALUED, though trending down from much higher levels. This indicates that stocks are too expensive relative to GDP).

You can track this and other indicators at: currentmarketvaluation.com.

Now, let’s get on with economic indicators for last week:

Keeping up with global economic data is a monumental task. With a financial planning and investment management firm to run, that is committed to doing our own independent research, we are forever grateful to the many excellent Economic aggregation resources that take the work out of gathering this data for us each day. They don’t give us analysis – that’s our job – but just compiling this information can be a full-time job. We want to give a big shout-out (and a thank you) to CurrentMarketValuations, FRED, MacroMicro, TradingEconomics, and The Daily Shot. Though we use several more, these are three of our favorite places to see a daily aggregation of economic data, and you’ll often see their charts used here.

- nFocus: The war in Israel

- Changes in our Economic Reporting (starting next week)

- General Economic Statement (since our last update)

nFocus: The war in Israel

War is hell and many thousands of people caught in the middle of a geopolitical and religious struggle will suffer tremendous losses. We don’t want to reduce the horrific events in Israel and Gaza over the weekend to economic or financial terms by any means, but we do want to look at the possible ramifications for the investing decisions we make for our clients as this is the purpose of these weekly updates.

A war in the Middle East, particularly one with multiple fronts, poses a significant risk of instability on the free flow of oil from the region. Right now we do not know of any mining of straits or seas near the combat area, or of patrolling ships not allowing the movement of oil tankers, but should that happen, we will see a tightening of oil supplies across many parts of the world, including the United States, further escalating prices of energy.

We may also see additional deficit spending by the United States government to now support wars on two fronts: Ukraine and Israel. We already have a worsening fiscal crisis, as the U.S. has added $2.1 TRILLION to the nation’s debt, just since June’s debt ceiling votes in Congress.

Gold should also spike temporarily, as instability grows, and we would expect a negative stock market reaction to these events with the possible exception of defense companies and energy produced stateside.

These events will obviously have an outsized impact on economic output in the region, and our deep ties to the Middle East may cause ripple effects here in the United States. We are watching it closely and will update our blog as conditions warrant.

Changes in our Economic Reporting (starting next week)

We’ve been revamping our economic and market reporting for our clients and blog readers over the past few weeks (that’s why we’ve been quiet) in this space, and wanted to share the new format with our readers this week.

Starting Monday, October 16:

- Our website will have a comprehensive page of real-time economic and market data available on the main menu of the site. This will provide raw feeds of the data we feel is most important for our own investing decisions relative to our client models. This page will not have any analysis of the data; it will simply be the most recent reads of important market and economic information as of the minute you read it. In order to keep this new content compliant with our industry regulators, no commentary from us will be provided (so our opinions on market situations don’t go out of date).

- Our Weekly Economic nSight posts will continue as you’ve come to expect them. This is where you will get our insight and analysis of what’s transpiring in the markets and economy over the past week, and what we believe it means about the trajectory of the economy. In addition to extensively covering the United States ‘ economy, the Weekly Economic nSight report will now also look at a different region of the economic world each week on a rotating basis, such as Canada, Europe and the UK, Asia, and Emerging Markets. Because of the interconnectedness of the economies of the world, an economic event in one country or region has a proportionate impact on others. We will also look at commodities and market dynamics as part of our weekly analysis.

What this means for you

We hope that you take this information and our analyses as helpful tools as you make personal and business financial decisions. The economy affects us all, and keeping informed about what’s changing can help us to make better decisions with our money, whether it’s saving, spending, or investing. This expansion of information, we hope, serves to deepen our clients’ understanding of the intimate connection between economic events and their investing returns, and how our firm is working to keep your money working – safely – toward your long-term goals.

General Economic Statement (since our last update)

Because of work we’ve been doing behind the scenes, plus the economy itself has continued along the same trajectory with little change so far, we opted to work internally on various client and regulatory work, and get our new market and economic dashboard ready for launch. That doesn’t mean we’ve taken our eye off of the economy by any means; simply that we allowed a couple of weeks to pass without reporting, essentially, the same information to our readers.

Bond Prices: The economy continues to cool and we are most worried at the moment about the stark drop in treasury bond prices, sending bond yields much higher over the last few weeks. This has happened just before market meltdowns in the last two recessions, as well. When no one is interested in buying treasury bonds, sending their prices down and yields up, it indicates that the market is betting on increasing rate hikes in the near future.

The bigger concern about bond prices falling is that the holders of current bonds (and that’s the vast majority of U.S. banks in particular) are watching the resale value of those bond holdings drop substantially. The money a bank’s customers deposit that is not lent out to borrowers is often held in U.S. Treasury bonds to earn a safe yield for the bank. If those bonds drop too much in value, the bank can be technically insolvent relative to its reserve requirements. Combined with the rising delinquency rates on car, home and business loans these banks have lent out, and we may have some bank liquidity problems, and even bank failures, before the economy is trending up again. We are watching this closely.

Prices / CPI: Bond price drops is what we would expect if investors believed the Fed was not doing enough yet to curb inflation. And indeed, prices have turned the corner and started to reverse higher again after a year of declines. As we’ve said many times in this space, inflation tends to run in waves, and just when you think you might have it beaten (and therefore take your foot off of the economy’s brake prematurely), it can turn around and run up again, which it looks like it wants to do. We are 75% confident of at least one more Fed hike as early as the November FOMC meeting, unless something “breaks” beforehand, like additional bank failures mentioned above.

However, if the Fed doesn’t stay the course until inflation is on a proven trajectory toward its 2% target, the Fed must then surrender to higher long-term inflation rates. So far, the Fed is adamant that they are committed to the 2% inflation target, and if we are to take them at their word, that means they must hold interest rates higher for longer than most market analysts believed. We’ve been telling our clients for over a year that we are in line with the Fed’s statements on the sticky nature of inflation and have had our clients invested for the “higher for longer” scenario since 2022.

Employment: Hiring remains strong – officially. However, I have lost much faith in the first announcements of new employment data from the Bureau of Labor Statistics for two reasons: first, because it is revised downward nearly every single time within a few weeks, and second, because only since 2021, the employment data from our government completely decoupled from another employment report published by ADP. These two reports ran tightly together for many years, and only since 2021 has the BLS data completely disconnected from ADP. Because ADP is not having to issue substantial revisions to its data on a continual basis, but the government data does so after nearly every print, I now believe the BLS data is intentionally erroneous at first print for political reasons. We therefore look at ADP data and the subsequent REVISIONS of the BLS data, but not the first data announcement that grabs all of the media attention.

It is important to know that hiring typically remains strong right into the beginning of a recession, and then drops rapidly during. Indeed, layoff announcements are up significantly in the past two weeks, as are continuing unemployment claims, which we’ve talked about repeatedly in this space. We continue to believe that as the recession finally grabs hold in as little as 90 days, the official employment information will naturally reverse and trend lower.

Real Estate: we continue to believe real estate is going to be one of the major factors in how significant this recession gets. Commercial real estate is deep in recession already, and residential real estate is not far behind as mortgage rates have hit 8% for the first time since the early 1990s. We will have much more on this next week.

What this means for you

We see nothing to change our view of the worsening economic trajectory we’ve talked about many times in this space. We will resume with deeper data dives in these and other subjects next week.

Bottom Line:

Download our brand-new E-Book “7 Hacks To Recession-Proof Your Financial Life” today.

We remain convinced that a recession is imminent, even as the market fights back hard against it. Do not let the current market rally fool you – there is no sustainable way to grow profits (and therefore a supportable stock price) in an economy that is rapidly losing steam. Corporate profit reports are backward-looking and economic projections are forward-looking. Do not be lulled into complacency just because the stock market allows itself to.

We’ve been alerting our clients for nearly two years now that inflation was going to cause significant problems and our central banks would have to take progressively stronger actions to combat it. That appears to be a correct call.

No one knows exactly when a recession will be declared, but we firmly believe most of the larger economies of the world are right at the door of one now. Recessions can take years to recover from, which is why we believe it is vitally important to get your family and business finances ready to weather through such a storm.

We predicted the beginning of a turn in the current market rally last week, and we reiterate that sentiment now. There will always be market movement that runs counter to the economic data because markets are much more short-term focused, and let’s face it: until fear takes hold, greed is the prevailing emotional state of most market participants. We do believe, however, that the recent rally has fully run its course, and there will soon be a strong shift from stocks into safer investment options such as corporate and government bonds. With interest rates this high, getting a 5% or better yield, risk-free is becoming a more and more attractive option for investors concerned about the coming economic uncertainty. Once there is consensus that either the economy is earnestly deteriorating, or the Fed announces the end of rate hikes, the move from stocks to bonds will accelerate.

Whether you are our client or not, you need to consider the broader economy (and much less so the daily market fluctuations) when making investment decisions. The economy is telling us clearly what is coming, and you need to have your investment accounts prepared before that happens.

Just this past spring, I published an ebook to help you get your finances ready for the recession directly ahead. It’s yours totally free. Just click on the book image to access and download it.

Use these economic reports, and those of others working in this space, to prepare. You can not only avoid much of the pain that is coming, but you might actually profit from it, if your investments are properly positioned, and you’ve done what you can to shore up your business’ and family’s financial situation. If you need help with this, nVest Advisors has amazingly affordable personal financial planning and fiduciary investment management services to help you.

This is what we do for a living, and we’re very happy to partner with you on that endeavor.

Reach out to us for a totally free financial and portfolio checkup today if you’re concerned about where your finances sit for the coming few years, particularly if you are at or approaching retirement age. We’re delighted to offer you our thoughts. You can schedule that time with us below:

Watching This Week:

- Jobs Report

- Service Sector Update

- Commodities

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]

Jeremy Torgerson, CEO, CIO & Senior Advisor